Executive summary

AI has exploded onto the scene, capturing the imagination of the public and investment community alike, and with many seeing it as transformative in driving future economic growth. Certainly, it’s finding its way into all manner of devices and services.

But its thirst for data and generative capabilities across all modalities (text, images, audio, video etc.) will drive a need for a more hyperconnected compute fabric encompassing sensing, connectivity, processing and flexible storage. Addressing these needs will likely be dependent on a paradigm shift away from just connecting things, to enabling “connected intelligence”. Future networks will need to get ‘smarter’, and will likely only achieve this by embracing AI throughout.

Emergence of AI

Whilst AI has been around for 70 years, recent advances in compute combined with the invention of the Transformer ML architecture and an abundance of Internet-generated data has enabled AI performance to advance rapidly; the launch of ChatGPT in particular capturing worldwide public interest in November 2022 and heralding AI’s breakout year in 2023.

Many now regard AI as facilitating the next technological leap forward, and it has been recognised as a crucial technology within the UK Science & Technology Framework.

But how transformative will AI really be?

Sundar Pichai, CEO Alphabet believes “AI will have a more profound impact on humanity than fire, electricity and the internet”, whilst Bill Gates sees it as “the most important advance in technology since the graphical user interface”.

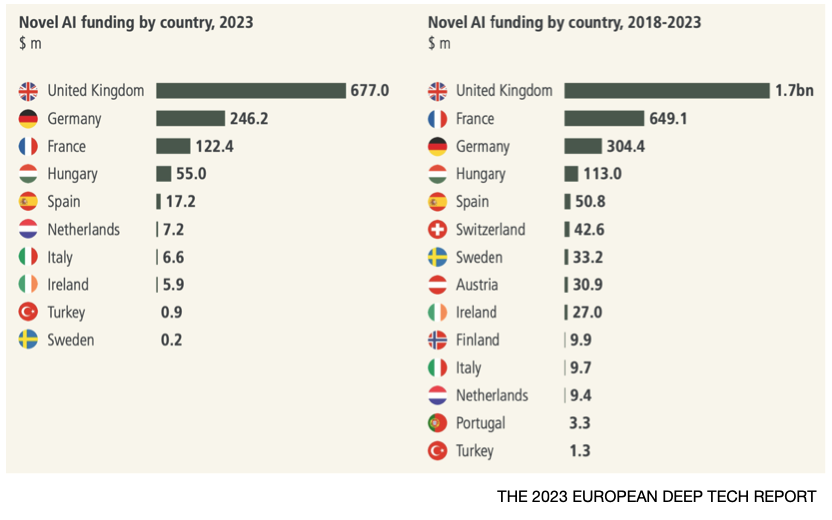

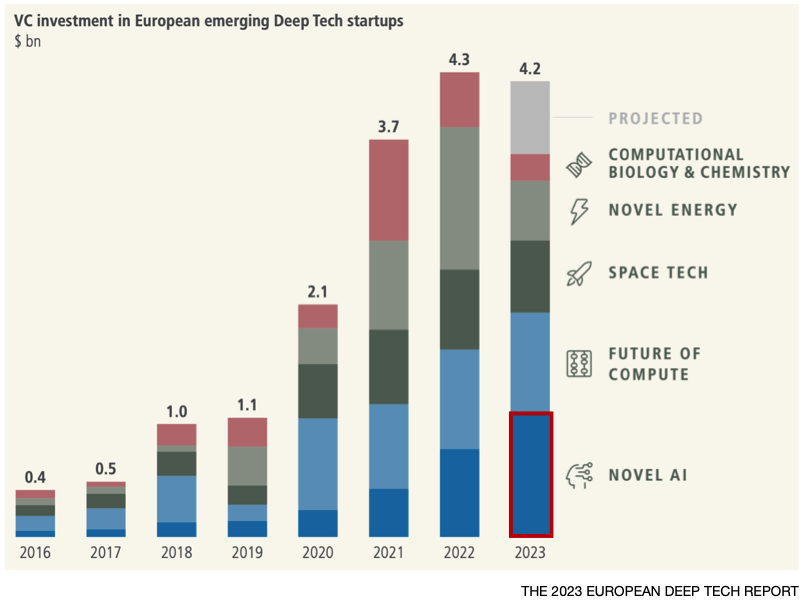

Investor sentiment has also been very positive, AI being the only sector within Deep Tech to increase over the past year, spurred on by the emergence of Generative AI (GenAI).

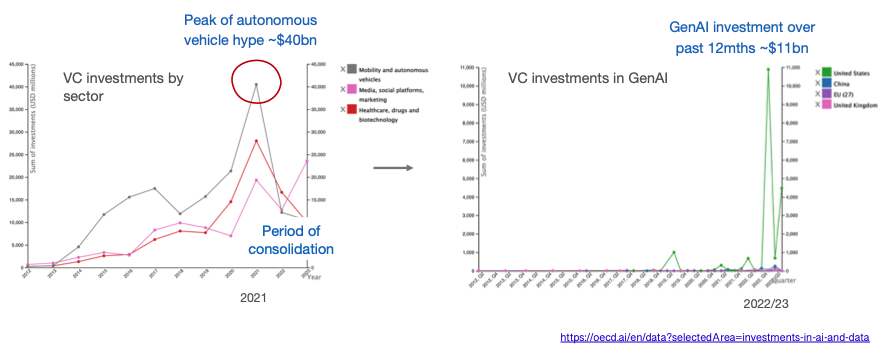

But is GenAI just another bubble?

The autonomous vehicle sector was in a similar position back in 2021, attracting huge investment at the time but ultimately failing to deliver on expectations.

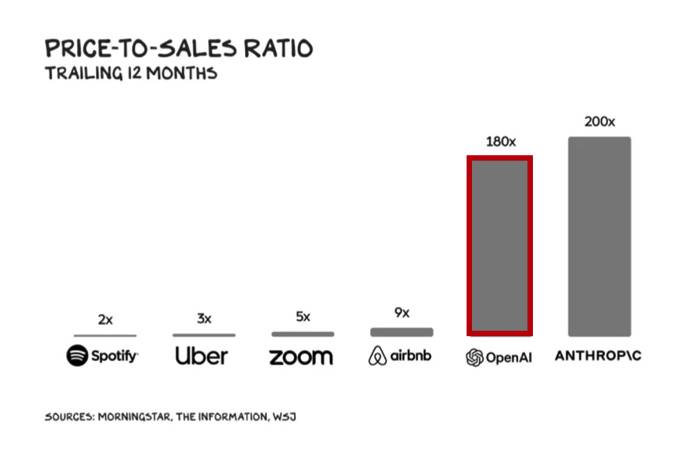

In comparison, commercialisation of GenAI has gotten off to an impressive start with OpenAI surpassing $2bn of annualised revenue and potentially reaching $5 billion+ this year, despite dropping its prices massively as performance improved – GPT3 by 40x; GPT3.5 by 10x with another price reduction recently announced, the third in a year.

On the back of this stellar performance, OpenAI is raising new funding at a $100bn valuation ~62x its forward revenues.

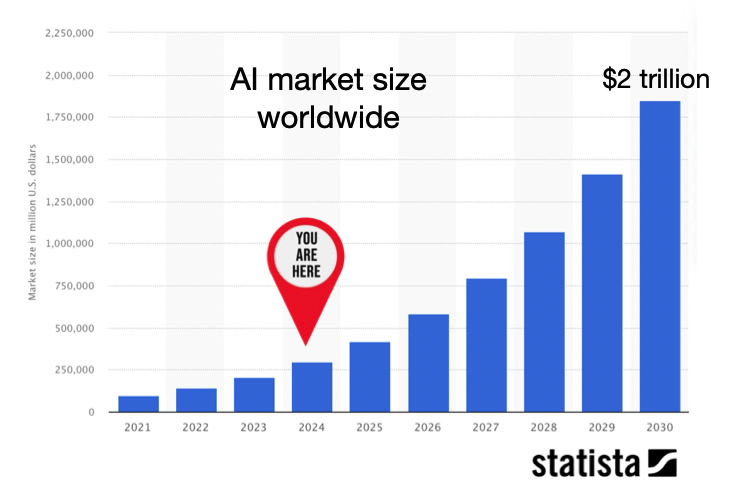

Looking more broadly, the AI industry is forecast to reach $2tn in value by 2030, and contribute more than $15 trillion to the global economy, fuelled to a large extent by the rise of GenAI.

Whilst undeniably value creating, there is concern around AI’s future impact on jobs with the IMF predicting that 40% may be affected, and even higher in advanced economies. Whether this results in substantial job losses remains a point of debate, the European Central Bank concluding that in the face of ongoing development and adoption, “most of AI’s impact on employment and wages – and therefore on growth and equality – has yet to be seen”.

Future services enabled/enhanced by AI

Knowledge workers

GenAI has already shown an impressive ability to create new content (text, pictures, code) thereby automating, augmenting, and accelerating the activities of ‘knowledge workers’.

These capabilities will be applied more widely to the Enterprise in 2024, as discussed in Microsoft’s Future of Work report, and also extend to full multimodality (text, images, video, audio etc.), stimulating an uptick in more spatial and immersive experiences.

Spatial & immersive experiences (XR)

The market for AR/VR headsets has been in decline but likely to get a boost this year with the launch of Meta’s Quest 3 and Apple’s Vision Pro ‘spatial computer’.

Such headsets, combined with AI, enable a range of applications including:

- Enabling teams to collaborate virtually on product development

- Providing information for engineers in the field – e.g., Siemens and Sony

- Simulating realistic scenarios for training purposes (such as healthcare)

- Showcasing products (retail) and enabling new entertainment & gaming experiences

The Metaverse admittedly was over-hyped, but enabling users to “see the world differently” through MR/AR or “see a different world” through VR is expected to boost the global economy by $1.5tn.

Cyber-physical & autonomous systems

Just as AI can help bridge the gap for humans between the physical and the digital, GenAI can also be used to create digital twins for monitoring, simulating and potentially controlling complex physical systems such as machinery.

AI will also be used extensively in robotics and other autonomous systems, enhancing the computer vision and positioning & navigation (SLAM) of smart robots in factories, warehouses, ports, and smart homes with predictions that 80% of humans will engage with them daily by 2030.

Personal devices

And finally, AI is already prevalent in many personal devices; in future, “Language models running on your personal device will become your very personal AI assistant”.

Connected Intelligence

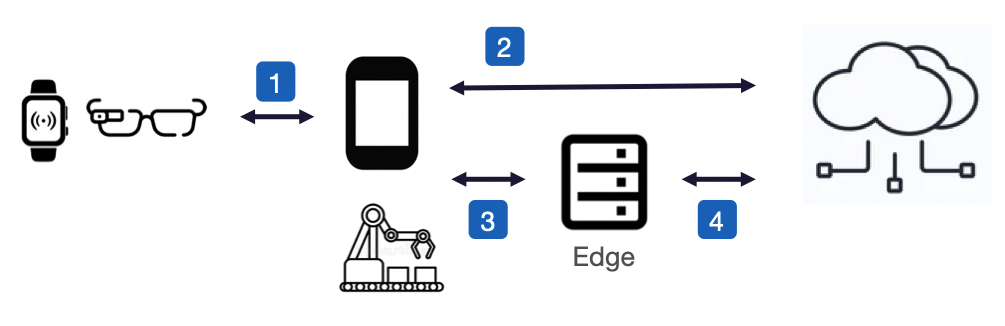

These future services will drive a shift to more data being generated at the edge within end-user devices or in the local networks they interface to.

As the volume and velocity increases, relaying all this data via the cloud for processing becomes inefficient, costly and reduces AI’s effectiveness. Moving AI processing at or near the source of data makes more sense, and brings a number of advantages over cloud-based processing:

- improved responsiveness – vital in smart factories or autonomous vehicles where fast reaction time is mission critical

- increased data autonomy – by retaining data locally thereby complying with data residency laws and mitigating many privacy and security concerns

- minimising data-transfer costs of moving data in/out of the cloud

- performing continuous learning & model adaptation in-situ

Moving AI processing completely into the end-user device may seem ideal, but presents a number of challenges given the high levels of compute and memory required, especially when utilising LLMs to offer personal assistants in-situ.

Running AI on end-user devices may therefore not always be practical, or even desirable if the aim is to maximise battery life or support more user-friendly designs, hence AI workloads may need to be offloaded to the best source of compute, or perhaps distributed across several, such as a wearable offloading AI processing to an interconnected smartphone, or a smartphone leveraging compute at the network edge (MEC).

Future networks, enabled by AI

Future networks will need to evolve to support these new compute and connectivity paradigms and the diverse requirements of all the AI-enabled services outlined.

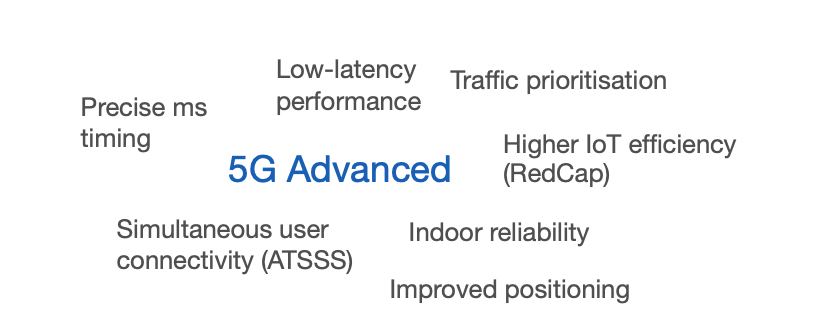

5G Advanced will meet some of the connectivity needs in the near-term, such as low latency performance, precise timing, and simultaneous multi-bearer connectivity. But going forward, telecoms networks will need to become ‘smarter’ as part of a more hyperconnected compute fabric encompassing sensing, connectivity, processing and flexible storage.

Natively supporting AI within the network will be essential to achieving this ‘smartness’, and is also the stated aim for 6G. A few examples:

Hardware design

AI/ML is already used to enhance 5G Advanced baseband processing, but for 6G could potentially design the entire physical layer.

Network planning & configuration

Network planning & configuration is increasing in complexity as networks become more dense and heterogeneous with the move to mmWave, small cells, and deployment of neutral host and private networks. AI can speed up the planning process, and potentially enable administration via natural language prompts (Optimisation by Prompting (OPRO); Google DeepMind).

Network management & optimisation

Network management is similarly challenging given the increasing network density and diversity of application requirements, so will need to evolve from existing rule-based methods to an intent-based approach using AI to analyse traffic data, foresee needs, and manage network infrastructure accordingly with minimal manual intervention.

Net AI, for example, use specialised AI engines to analyse network traffic accurately in realtime, enabling early anomaly detection and efficient control of active radio resources with an ability to optimise energy consumption without compromising customer experience.

AI-driven network analysis can also be used as a more cost-effective alternative to drive-testing, or for asset inspection to predict system failures, spot vulnerabilities, and address them via root cause analysis and resolution.

In future, a cognitive network may achieve a higher level of automation where the human network operator is relieved from network management and configuration tasks altogether.

Network security

With the attack surface potentially increasing massively to 10 million devices/km2 in 6G driven by IoT deployments, AI will be key to effective monitoring of the network for anomalous and suspicious behaviour. It can also perform source code analysis to unearth vulnerabilities prior to release, and thereby help mitigate against supply chain attacks such as experienced by SolarWinds in 2020.

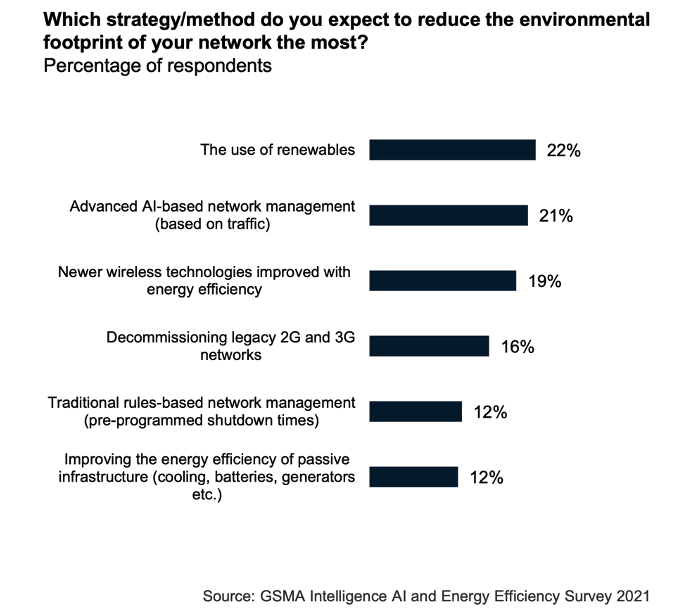

Energy efficiency

Energy consumption can be as high as 40% of a network‘s OPEX, and contribute significantly to an MNO’s overall carbon footprint. With the mobile industry committing to reducing carbon emissions by 2030 in alignment with UN SDG 9, AI-based optimisation in conjunction with renewables is seen as instrumental to achieving this.

Basestations are the ‘low-hanging fruit’, accounting for 70-80% of total network energy consumption. Through network analysis, AI is able predict future demand and thereby identify where and when parts of the RAN can be temporarily shut down, maintaining the bare-minimum network coverage and reducing energy consumption in the process by 25% without adversely impacting on perceived network performance.

Turkcell, for example, determined that AI was able to reduce network energy consumption by ~63GWh – to put that into context, it’s equivalent to the energy required to train OpenAI’s GPT-4.

Challenges

Applying AI to the operations of the network is not without its challenges.

Insufficient data is one of the biggest constraints, often because passive infrastructure such as diesel generators, rectifiers and AC, and even some network equipment, are not IP-connected to allow access to system logs and external control. Alternatively, there may not be enough data to model all eventualities, or some of the data may remain too privacy sensitive even when anonymised – synthesising data using AI to fill these gaps is one potential solution.

Deploying the AI/ML models themselves also throws up a number of considerations.

Many AI systems are developed and deployed in isolation and hence may inadvertently work against one another; moving to multi-vendor AI-native networks within 6G may compound this issue.

The AI will also need to be explainable, opening up the AI/ML models’ black-box behaviour to make it more intelligible to humans. The Auric framework that AT&T use for automatically configuring basestations is based on decision trees that provide a good trade-off between accuracy and interpretability. Explainability will also be important in uncovering adversarial attacks, either on the model itself, or in attempts to pollute the data to gain some kind of commercial advantage.

Skillset is another issue. Whilst AI skills are transferable into the telecoms industry, system performance will be dependent on deep telco domain knowledge. Many MNOs are experimenting in-house, but it’s likely that AI will only realise its true potential through greater collaboration between the Telco and AI industries; a GSMA project bringing together the Alan Turing Institute and Telenor to improve Telenor’s energy efficiency being a good example.

Perhaps the biggest risk is that the ecosystem fails to become sufficiently open to accommodate 3rd party innovation. A shift to Open RAN principles combined with 6G standardisation, if truly AI-native, may ultimately address this issue and democratise access. Certainly there are a number of projects sponsored within the European Smart Networks and Services Joint Undertaking (SNS JU) such as ORIGAMI that have this open ecosystem goal in mind.

Takeaways

The global economy today is fuelled by knowledge and information, the digital ICT sector growing six times faster than the rest of the economy in the UK – AI will act as a further accelerant.

Achieving its full potential will be dependent on a paradigm shift away from just connecting things, to enabling “connected intelligence”. Future networks will need to get ‘smarter’, and will likely only achieve this by embracing AI throughout.

The UK is a leader in AI investment within Europe; but can it harness this competence to successfully deliver the networks of tomorrow?